Yield farming on a potential future tech darling because I'm too scared to BTFD

Yield farming on a potential future tech darling because I'm too scared to BTFD

Welcome back to me. First idea/trade in a while. Pour up a TOST to your boy Elmer.

Hello all. Between surviving busy season, working on finding my next career opportunity, navigating these finally-more-interesting markets, brief jaunts to Puerto Vallarta and Whistler, and a general lack of good (if I’m being generous to myself) ideas… it has been a while. I’m back with the first of hopefully a few trade/investment ideas and introspective posts.

Today’s topic - a tech company that I really, really like (but am not super confident about the valuation of the stock) and how I am choosing to play this situation.

The stock: Toast (TOST).

If you’ve had the pleasure of encountering them in the wild, you’ve probably been wowed at how good the technology/experience works (for the customer). My first experience was years ago at Dos Toros (a NYC quick service Mexican chain that is 10x better than Chipotle), where the little Toast card reader widget processed the chip card virtually instantaneously (back when all others, and still today many others, take 5-10-15 seconds to complete the transaction).

More recently, many of my favorite mom-and-pop restaurants in Seattle have waitstaff using Toast handheld terminals - they can be used for order-taking and tableside payment. Sure, Europeans may have had (a simpler form of) this when I went to Sweden in 2017, but this is still a rarity in the United States with Toast blazing the trail. I always feel bad being that guy when I ask, but I do ask pretty much every server using one how they like it, and I am yet to not get a rave review. It makes order-taking easier, helps with speed and kitchen accuracy, and most importantly eliminates the traditional payment musical chairs (print check, often don’t take the card immediately because that would be uncouth, come back 5 minutes later to collect the credit card, go run the credit card, bring it back - a fun 10 minute process at the end of a hopefully delicious meal which annoys the customer and slows tables turning).

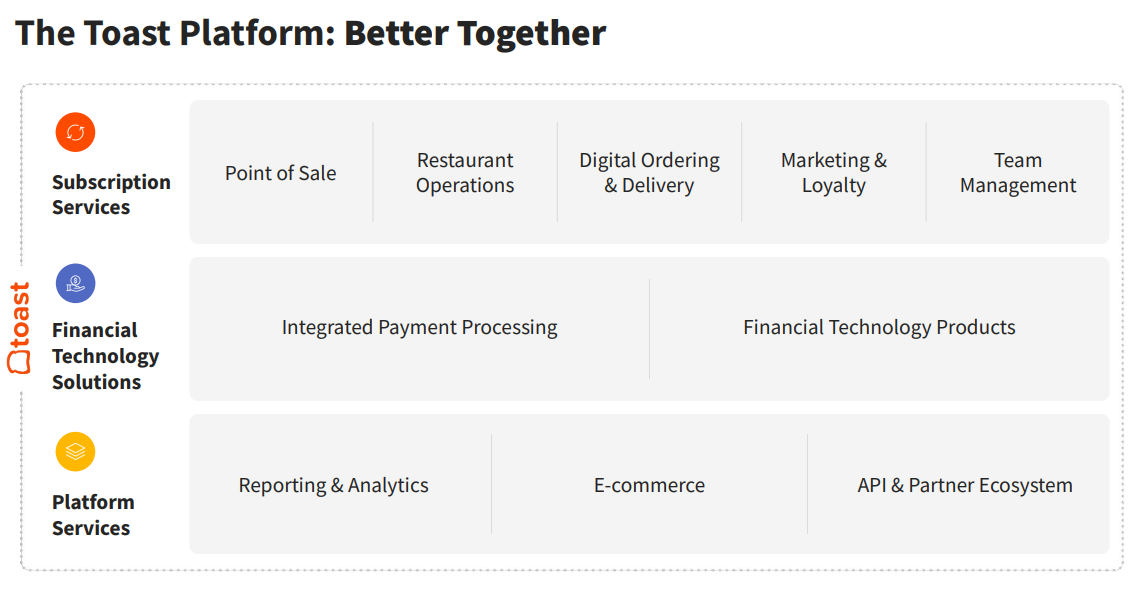

But Toast is more than just these little handheld terminals. They are/can also be the restaurant’s ERP system - providing point of sale systems, processing payments, integrating with online orders and delivery (critical in our continual-COVID world), and more.

So those are the basics. Here’s their most recent quarterly presentation if you want a bit more background. But now onto the opportunity, dilemma, and trade.

The opportunity:

I think TOST will continue to gain market share as, from my experience and from the research and testimonials I have gathered, it is truly leaps and bounds better than (generally dinosaur) competitors. My father (a very good but often Buffett-esque investor) has lamented at times that he should have bought stock in relatively nascent companies when he first encountered and enjoyed their products - e.g. Toyota/Honda when he was buying their cars for the first time, or Apple when all of our California cousins bought iPhones. This may be that moment here (or of course, it may not be). But Toast seems to have a superior product in an industry that is ripe for disruption (seriously why are servers still carrying cards back to physical registers to run them - and that is not even scratching the surface of other greater efficiencies, upsized checks, better delivery operations, etc. that the Toast product can lead to) - and that historically can be a very winning formula.

The dilemma:

Valuation. Toast is worth about $10b as of close on March 16th. In 2021, they did revenue of $1.7b, so they’re trading at about 6x sales, but that includes a bunch of revenue from payment processing which is pretty low margin. They did about $400m of gross profit in 2021 - 25x gross profit is pretty rich even for high growth. They are yet to be sustainably profitable on even an EBITDA basis (let alone GAAP net income). Sure, they should scale quite a bit over the coming years, but it’s hard to model out (mentally, I don’t do real models) how 2x or 5x revenue growth will translate into profitability.

TOST IPO’d during frothier days in late 2020 and traded around $50-60/share (~$30b market cap) for quite some time before coming back to earth along with the rest of tech garbage over the past few months. So, it looks like a relative bargain compared to where it was, but it’s still working to find footing in the high teens and I for one cannot say that $10b is the correct current valuation. If we return to frothier times, it could easily double and the company’s prospects may (when looking through rose-tinted glasses) support such valuation. If tech froth corrects further, it could halve. But I would be very comfortable owning it at $10, or about 3x revenue and 10x gross profit, much more reasonable for a quickly growing and what I think is a potentially revolutionary company. Which brings us to…

The trade:

Since I’m not confident that TOST is a bargain at ~$18, I’ve taken a toe-in-the-water approach to being fairly bullish - by selling puts.

If you’re not already familiar with selling puts as a bullish strategy, I would recommend that you close this article right now and perhaps consider buying a share or two to track TOST. No offense to the noobs, but I don’t want to be responsible for any damage arising out of discussing a more complicated options strategy. (seriously close it now)

If you are still reading -

I’ve been selling June 12.5 puts and December 7.5 puts over the past week or so. As noted above, I think that $10 is a pretty attractive bad-case valuation at which I’d like to own the stock, and I think that the chance of the Junes getting called away is fairly slim (but OK to me if it happens) and December is near nil.

June $12.5s are going for about $1.30 - if shares fall 33%, you’ll own the stock at ~$11. If shares don’t, you’ll generate a ~40% annualized yield (~$1.30 / $11.20 cash secured margin “outlay” * 4 as these expire in 3 months).

December $7.5s currently go for a bit under a dollar (I sold a few for over a dollar yesterday, but TOST recovered along with the tech trash today and the option price fell). These “yield” close to 20% (~$0.90/$6.6 margin * 4/3 for the 9 months remaining). I think the chance of it going below $7.5 is near zero, but if it does, I would be buying hand over fist at $6.6 anyway.

So, that’s about it. I like Toast’s prospects a lot. I am not sure whether $18 is the right price to buy into the growth potential today, given market/tech fluctuations, but I am quite comfortable owning it around $10, so instead of buying shares, I’m selling puts to either get free money or buy it at that price plus a bit of a discount.

I hope you enjoyed and I hope to have more for you here shortly.

Yours truly,

Elmer