Tails I Lose, Heads I Make 10x (maybe).

Tails I Lose, Heads I Make 10x (maybe).

This is what SPAC Warrants were designed for.

SPACs, for good reason, have gone from being the hottest corner of the market to the red-headed stepchild over the past year … so, there is now plenty to sift through in the minefield. Plenty of de-SPACs have been total complete trash (looking at you, MILE), while others are legitimate businesses that have a bit of a grey cloud hanging overhead.

Anyway, to the uninitiated, one of the other features of SPACs is that most of them have warrants. These warrants typically operate as a (typically) five-year call option, as they provide the warrantholder the right to obtain a share at a specified price, typically $11.50. They are also callable/redeemable by the Company based on certain specified conditions, typically when the Company trades above a certain price for a given period of time (20 or 30 days).

So, SPAC warrants are essentially LEAP calls (and the underlying SPACs often do not have any calls or limited chains), so they can be helpful in making leveraged directional bets on the Company eventually finding its footing.

And, without further ado, here is a particular former SPAC, with warrants, that I believe presents an unique opportunity to bet on what is, hypothetically, a binary outcome - the underlying company succeeding in the plan that it has laid out. And no, this is not a typical SPAC definitive agreement hockey-stick “TAM of the entire world” promise - this is a tangible plan.

The Company? Brooge Energy.

The shares trade as BROG and the warrants, which are the focal point of this idea, trade as BROGW.

Credit where credit is due - this idea is a derivative of this extremely informative overview of the general bull case, published on Seeking Alpha, linked here. I would suggest reading it as overall background (though I will provide some below) but I also want to give fair credit to the author who put in the work (and I would have not had this trade idea if it wasn’t for his article).

So, a bit of background:

Brooge operates an oil storage facility in the United Arab Emirates (Fujairah, one of the less name-brand ones). But, importantly, Brooge’s facility is on the eastern side of the UAE, past the Strait of Hormuz, one of the chokepoints in the global oil trade and an area where geopolitical tensions sometimes get a bit heated.

Now, here’s the real basis for the idea:

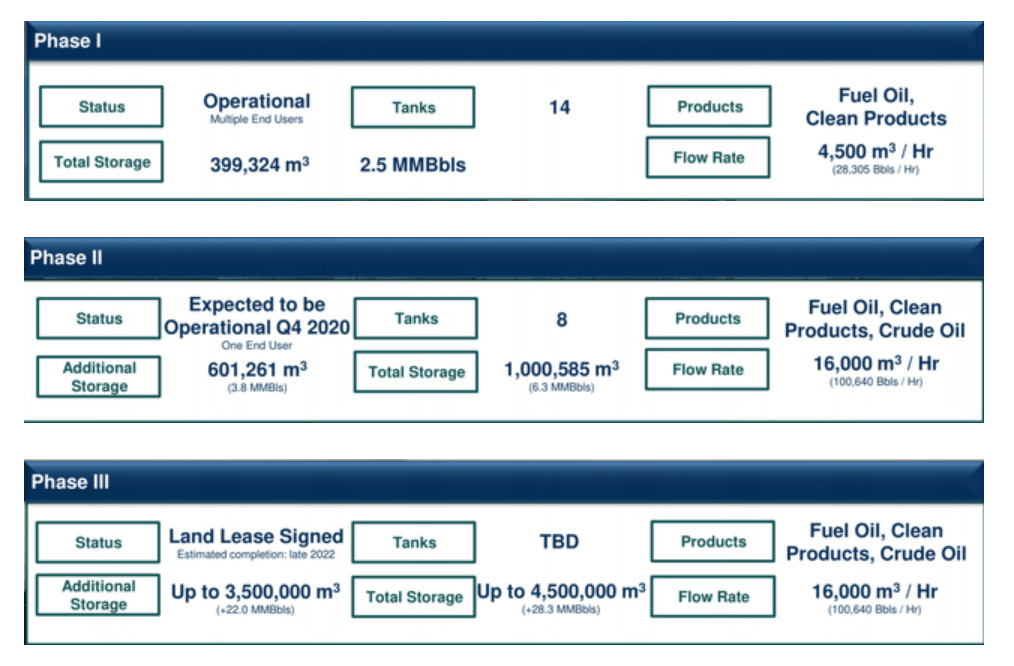

Brooge has opened in phases. Its Phase I operations began all the way back in December 2017 and have been running reliably since, producing a respectable amount of income. Phase II has recently become operational, and significantly increased the scope of operations. But Phase III is what we really care about.

Phase 3 will nearly quadruple total storage, and therefore, potential income. Work has begun with permitting in place, trending towards completion/operations beginning in late 2022 or early 2023.

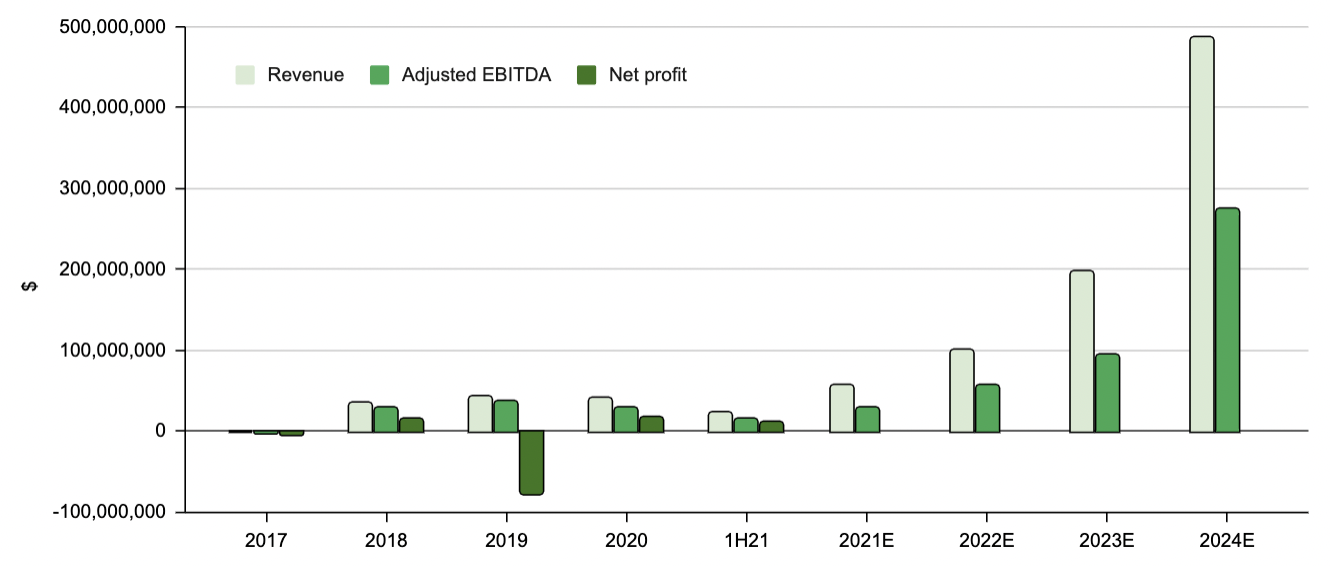

And with that, per the Company’s forecast (compiled by the author of the linked Seeking Alpha article), earnings are expected to increase tremendously.

The Company currently trades at an enterprise value of about $1.2 billion. Such valuation clearly bakes in some future success, and that valuation may likely grow (but not to the benefit of current equity holders) as it takes a few hundred million dollars in equity or debt issuance to build out Phase III operations, but it does not nearly bake in the full potential (which I will articulate below is not no-risk, but may not be high-risk). If the Company does manage to meet its forecasts, throwing off $300m+ of EBITDA 3-4-5 years from now, the equity will likely trade at ~10-15x EBITDA, or $3-5 billion.

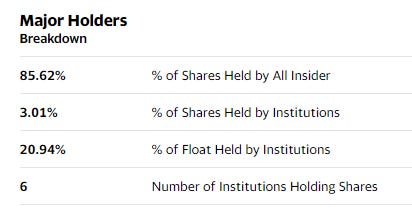

Why are these pipe dreams even worth dignifying? Well, as the Seeking Alpha author notes (and I do not have the tools to personally corroborate or refute), ~80% of shares are held by “UAE dignitaries” and I for one trust the Emiratis, despite having plenty of money, probably want to see their investments succeed.

So, enough about the background - here’s how I’m playing it:

As noted, BROG has warrants (which trade as BROGW) which the clock started ticking on in September 2019, which means that they turn into a pumpkin in September 2024. The warrants currently trade for about 60 cents. They are redeemable if/when BROG trades for $18 or more for 20 out of 30 days (which does not directly cap upside, but may mean its time to sell or else convert to shares, which will require an $11.50 capital outlay for every 60 cents spent now).

But, if the Company executes on its plan, which I think it has a solid? decent? possible? certainly non-zero chance of doing so, and does so more or less on the prescribed timeline (which provides a bit of room for comfort but not as much as one would love in this post-pandemic tight-supply-chain-world), BROG common could easily double as Phase III comes online and the Company begins printing money. In that case, I’d expect BROG common to exceed the $18 (just using for sake of the triggering event), in which case today’s 60 cent warrants would be worth $6.50 (or more) each. Given that this is basically a binary event - the Phase III operations happening, or not - I think of this as I think of my beloved options spreads, but in a different way. Even if this has a 75% chance of not working out (and the common staying below $11.50 forever), but at 25% chance of working out, the expected return is still 2.5x (.25*$6.50 + .75*0 = $1.62, vs. today’s warrant price of ~$0.60).

An important trading note: the warrants are quite thinly trade (as is the underlying, but the warrants even more so) so to the extent you may be intrigued by the idea, be very careful entering - can’t just put in a market order for a bunch of them, or else you are going to get a bad price.

And it is worth noting that the upside at that point is not capped - one can certainly exercise the warrants as a de-risked but still getting going company that will be spitting off cash which may be trading at $20 at the time of warrant redemption may end up going to $30 or $40 and paying a few bucks a share in dividends per year.

So, in conclusion, one more shoutout to the Seeking Alpha piece which was the basis for the idea, and my baggy brain for desiring to lever it up. As noted above, this is certainly far from guaranteed - there is geopolitical risk, execution risk, energy markets risk, you name it (which is one of the reasons why the common still trades at/a hair below the SPAC price and why the warrants are relatively cheap). There is also a good chance that between now and 2023/2024 when this potentially hits paydirt that investors get bored and warrants trade far lower than they do today - I’m putting on what I’ll tell myself is like a 70% position and see where things go from here - i.e. in mid-2022 if there are no negative developments but there is investor boredom and these trade for .40, the trade won’t be over yet but the risk/return will be even more attractive.

I plan to hold these warrants until they pry them from my hands - either because we got our 10 bagger and they get redeemed, or because this Phase III was all smoke and mirrors and my Ally Risk Manager deletes the expired derivates from my account sometime in late 2024.

As always, this is never advice, we’re just throwing 10x-ideas-spaghetti at the wall and seeing what sticks.

Yours,

Elmer