My favorite shitco microcap with a history of squeezing

My favorite shitco microcap with a history of squeezing

Read at your own risk.

Honestly its embarrassing for any company to have an $100 million market cap in this day and age. Just put Bitcoin or Crypto or SaaS or Green Energy or EV or Battery or something in your company’s name and you’ll be worth billions. But there is one little guy that I’ve been following for a while which I like to trade in and out of - and I am getting back in it.

It’s surprisingly a semi-household name but its unsurprisingly a crappy company. But, everything has its price.

The stock?

Blue Apron (APRN).

APRN came onto the market as a hot IPO - well done management and underwriters - and has since withered away to nothing as the food delivery box business has proved to not be that fantastic.

But in the past year and a half, it has squeezed and meme’d a few times.

I made a bit on the squeeze in early 2021, when other heavily shorted stocks and other generally garbage companies were spiking. I did so via a “ghetto spread” - first buying some calls naked, and eventually selling other calls against that position, and ended up making ~100% from the trade despite all options expiring worthless. (Which means I did not do a perfect job executing this, as I am sure the 13’s would have been worth a lot on 1/28 when I sold the 24s, but so it goes).

Lately APRN has returned to its historical bottom at ~$4. It bounced a bit today (9/3/21). There is no immediate catalyst other than the whims of the market on why it may go on another run, but after the following chart I will detail why there is actually some kind of alright fundamental basis to owning it.

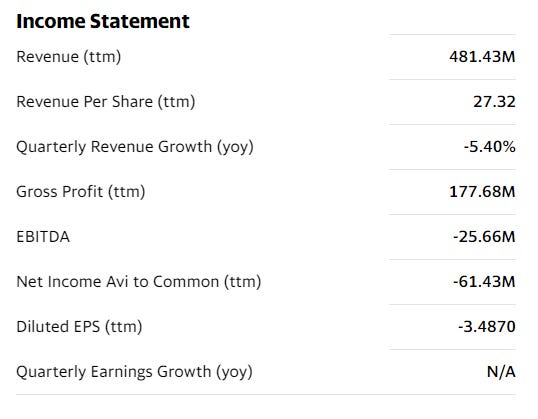

In some ways, APRN looks like it could be snapped up by an acquirer to buy cheap revenue and gross profit if they think they can make the business model work.

Enterprise value is about $100 million. Revenue is nearly $500 million. Gross profit is close to $200 million. Sure they lose money, but so does everyone in 2021.

So, this is a risky play based partially on charts and price action with some underlying financial backstop. There have been rumors of interest in acquisitions over the months/years with none coming to fruition so unlike HEAR, I do not truly believe that any deal is imminent. But you never know if a Walmart wants to take a swing at diversifying their e-commerce channels (as they did with Bonobos and Jet and others) and pays 1x gross profit for APRN, which would be an almost 100% premium.

Until then, it is a very small cap with little volume, some short interest (2 million shares which is about 2x average daily volume but 4x today’s volume) and a history of getting squeezy. Around its historical floor of $4, I like the speculative risk. I added some shares today (9/3/21) and will look to add more next week as well as examine options plays. As always, this is the opposite of advice.

-Elma